Is Rental Property Worth It? What Real Investors Actually Experience

Is Rental Property Worth It? What Real Investors Actually Experience

If you've owned a rental property for a few years and you're still waiting to feel like it was worth it — I want to tell you something important: you're not alone, and you're probably closer than you think.

The question of whether rental property is worth it comes up in almost every investor conversation I'm part of. And the honest answer is: it depends on what you're measuring, and what your timeline looks like. Because rental property wealth is not a sprint. It's one of the slower-burn, more durable ways to build real financial stability over time — if you understand the mechanics and you're patient enough to let them work.

Let's break down what's actually happening when you own a rental property — and why the first few years can feel like you're grinding uphill before you feel anything at all.

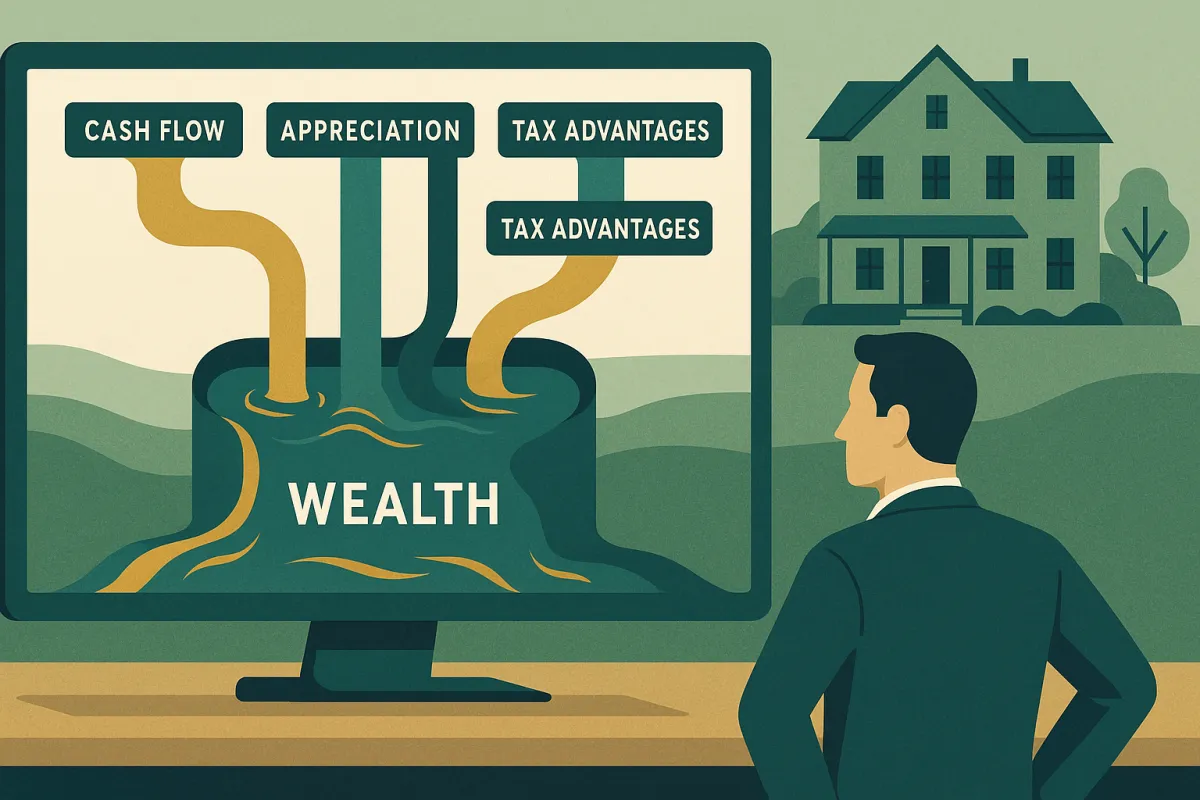

The Three (Really Four) Ways Rental Property Creates Wealth

Most people who buy a rental property are focused on one thing: the monthly cash flow check. And yes, cash flow matters. But rental property actually builds wealth through several channels simultaneously, and if you're only watching one of them, you're going to miss the full picture.

1. Cash Flow — Monthly Income After All Expenses

Cash flow is what's left over after you've paid your mortgage, property taxes, insurance, maintenance, vacancy allowance, and property management (if applicable). On a well-purchased rental in a stable market, you might clear $100 to $400 per month per property in positive cash flow. On a poorly purchased rental, you might be breaking even or running slightly negative.

Here's the thing: in the early years of ownership, many rental properties are cash-flow neutral or even slightly negative. Mortgage payments are highest relative to rent when you first acquire. But that's not the whole story.

2. Appreciation — The Slow Multiplier

Real estate appreciates over time. Not every year, not in every market, and not always on a predictable schedule — but historically, residential real estate tends to increase in value over long holding periods. A property you bought for $150,000 ten years ago may be worth $240,000 today. That $90,000 gain happened while someone else was making your mortgage payment.

Appreciation isn't income until you sell or refinance, which is why it can feel invisible — but it's real, it compounds, and it's one of the most powerful pieces of the wealth equation for long-term rental owners.

3. Loan Paydown — Your Tenant Builds Your Equity

Every mortgage payment reduces your loan balance. When your tenant pays rent, a portion of that payment flows through to reducing what you owe on the property. Over a 30-year mortgage, that paydown is dramatic. In the early years it's modest (most of your payment is interest). But after 10 or 15 years, the equity accumulation from paydown becomes meaningful — and it happened largely on someone else's dime.

4. Tax Advantages — Depreciation and Deductions

Rental property comes with a set of tax benefits that most other investments don't offer. Depreciation allows you to deduct the cost of the structure over 27.5 years, which can offset rental income on paper even when you're actually generating cash. Mortgage interest, repairs, insurance, and property management fees are all deductible. These advantages can meaningfully reduce your tax liability while the property builds value in the background.

Why "Is It Worth It?" Is Sometimes the Wrong Question

When someone asks if rental property is worth it, they're often really asking: "Am I making enough money right now to justify the hassle?" And that's a fair question. Managing tenants, dealing with repairs, navigating vacancies — there's real friction in this business.

But when you zoom out, the question changes. The better question is: "Am I building something that compounds over time?" And for most rental property owners who hold long enough and buy reasonably well, the answer is yes.

The challenge is that compounding wealth doesn't feel exciting in year two. It feels like work. The "this was worth it" moment tends to arrive later — when the mortgage is substantially paid down, when the property has appreciated, when the rent has increased with inflation while your fixed mortgage payment stayed the same, and when you suddenly realize the cash flow you're generating from a property that someone else essentially paid for over a decade.

What the First Five Years Usually Feel Like

Let me be straight with you about the early years, because I think a lot of would-be investors get discouraged and quit before they ever experience the payoff.

Years 1 and 2: You're dealing with the learning curve. Tenant issues you didn't expect. A repair that cost more than you budgeted for. Maybe a vacancy that stretched longer than planned. Cash flow might be minimal or nonexistent. You might genuinely be wondering if this was a mistake.

Years 3 and 4: The systems start working. You know your property better. You've found a maintenance person. Rents have crept up — but your mortgage payment hasn't. The cash flow is getting slightly better. The loan paydown is accumulating quietly in the background.

Year 5 and beyond: This is when most rental property investors start to exhale. The equity has grown. The net operating income has improved. And if you bought reasonably well and in a growing market, the value of the property may be meaningfully higher than what you paid.

Breaking Even Is Not the Same as Losing

One of the mental traps I see investors fall into is comparing rental property cash flow to the returns they see in the stock market — and concluding that breaking even on a rental is a failure. It isn't.

When you break even on a rental property, what's actually happening is: someone else is paying your mortgage, the property is (likely) appreciating, your equity is growing from loan paydown, and you're getting depreciation tax benefits. Breaking even on cash flow while all of those other forces are working in your favor is not a bad deal. It's actually a fairly good one.

Now, I'm not saying cash flow doesn't matter. It does. Negative cash flow is a real burden and you shouldn't ignore it. But the investors who look back 20 years and say "I wish I'd sold that rental" are rare. The ones who sold early because the early years felt unrewarding are the ones who regret it.

Rental Property vs. Other Investments

The honest comparison with index funds or equities is this: both have worked well over long holding periods. Index investing is simpler, more liquid, and requires zero property management. Rental property is less liquid, requires more active involvement, but comes with leverage, tax advantages, and inflation hedging that equity investing doesn't naturally provide.

Many of the most financially stable people I know hold both. They don't treat it as an either/or decision.

Who Rental Property Is NOT Right For

I believe in telling the full truth here. Rental property is not right for everyone, and I'd rather be straight with you than oversell an investment path.

Rental property may not be a fit if you need liquidity — rental real estate is not easy or quick to sell. It may not be right if you're unwilling to deal with any operational friction — tenants, repairs, and vacancies are part of the business. And it may not be right if you're buying in a market with poor fundamentals or paying above market to start with — the numbers have to make sense from the beginning.

But for folks who buy thoughtfully, hold long-term, and are willing to manage the early friction — rental property has been one of the most durable wealth-building vehicles available to regular people for a very long time.

The Bottom Line

The answer to "is rental property worth it" is almost always yes — but the timeline is longer than most people want to hear. The investors I've talked to who have owned properties for 15 or 20 years are almost universally glad they did. The ones who are frustrated tend to be three years in, measuring the wrong things, and not yet able to see what they're building.

Give it time. Run your numbers honestly from the start. Buy in markets with real fundamentals. And understand that the wealth in rental property doesn't announce itself every month — it compounds quietly until one day you look up and realize how much has accumulated.