Creative Financing 101: Buy Real Estate With Little or No Money Down

"I Don't Have Enough Money to Invest." — Let's Talk About That.

I hear this one constantly. And I understand why — if the only real estate transaction you've ever seen is a traditional purchase with a bank, 20% down, credit approval, and six weeks to close, then yeah — it seems like investing requires a lot of capital upfront.

But the traditional bank model is not the only model. It's just the most visible one. Investors who've been doing this for any length of time know that there's an entire category of deal structures that work when the traditional model doesn't — and some of those structures require very little cash to close.

This is what we call creative financing. And before you tune out thinking this sounds like a late-night infomercial, let me tell you what it actually is and how it actually works.

Here's What Most People Do Wrong

Most new investors assume that if they don't have the down payment, they can't invest. So they wait. They save. They think about investing while watching their target markets move. By the time they've saved enough for a traditional deal, they've lost years of market opportunity and deal volume.

Here's the thing: creative financing isn't a workaround or a desperation move. It's a legitimate set of tools that solves real problems for both buyers and sellers. A motivated seller who needs to get out from under a property might not care about getting all cash at closing — they might care about getting out of a bad situation fast, or generating monthly income, or avoiding a massive tax bill. Creative financing often solves those problems better than a traditional cash deal does.

The investors who know more tools close more deals. It's that straightforward.

Here's What I Do Instead

Here's what I do: I present every seller with multiple options. I never walk in with just one offer structure, because one structure rarely fits every situation. I present three versions — usually an all-cash offer (lower price), a subject-to offer, and a seller financing or agreement for deed offer — and I let the seller tell me which one fits their situation best.

That approach closes more deals. More options means more paths to yes.

Let me walk through the three main creative financing tools and when each one makes sense.

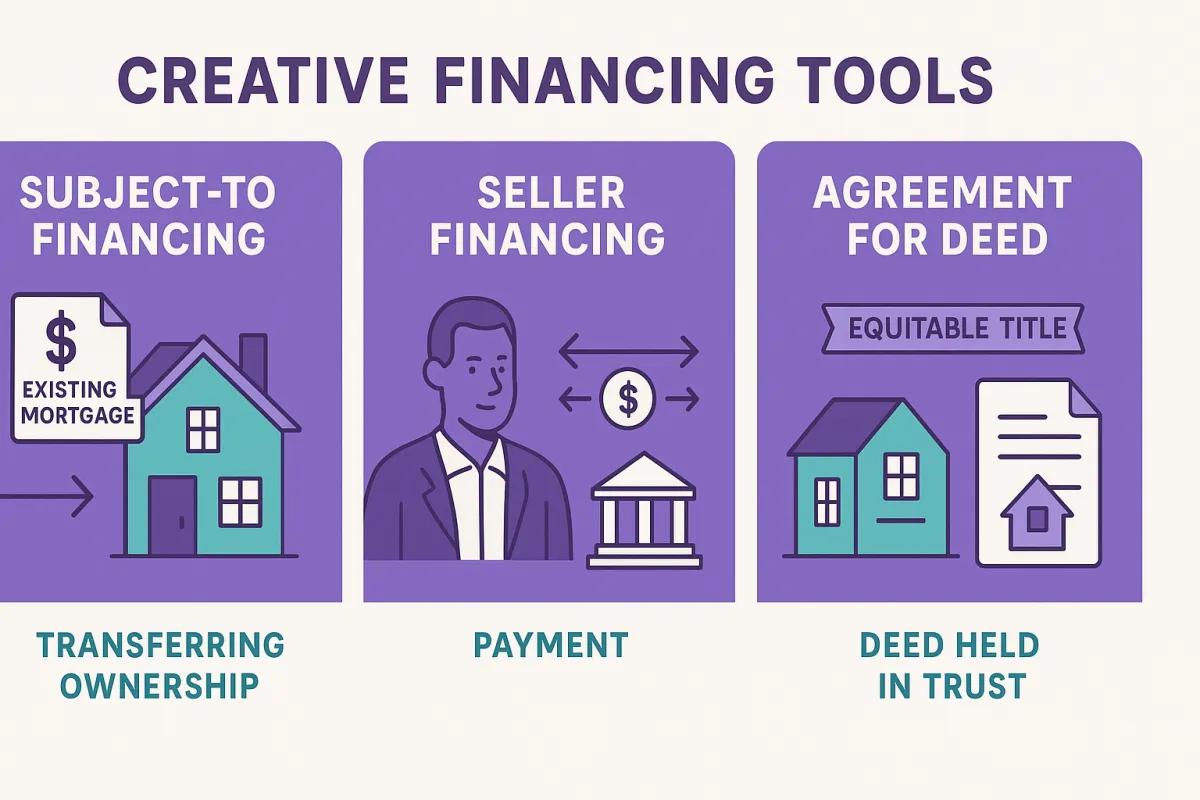

Tool 1: Subject-To Financing

Subject-to means you purchase the property subject to the existing financing. The seller's mortgage stays in place — in their name — and you take over making the payments. The deed transfers to you at closing. You own the property. You make the mortgage payment. The loan balance stays with the seller's bank.

Who this is best for:

- Sellers who are behind on payments and heading toward foreclosure

- Sellers with little or no equity who can't net enough from a traditional sale to cover closing costs

- Sellers who just need out fast and don't need a lump sum

- Situations where the existing loan has a favorable interest rate you'd love to keep

Let me give you an example. A seller bought their house in 2020 at a 3.25% interest rate. Life circumstances changed — divorce, job loss, whatever — and they're now two months behind. The house is worth roughly what they owe. A traditional sale leaves them with nothing, or worse. But a subject-to deal means you take over the payments, they walk away clean, you get a property with a 3.25% rate you could never get from a bank today. You rent it out at a rate that covers the payment plus expenses.

The seller gets out of their problem. You get a property with great existing financing terms. Done.

Critical rule: If you take over someone's mortgage payments, you make them on time every single time. That loan is in their name. A late payment hits their credit, not yours. That's a trust obligation — honor it.

Tool 2: Seller Financing (Seller Carryback)

In a seller-financed deal, the seller becomes the bank. You and the seller agree on a purchase price, down payment, interest rate, and term. You make monthly payments directly to the seller. The deed transfers at closing. You own the property.

This is different from subject-to because there's no existing bank mortgage involved — the seller owns the property free and clear (or close to it) and is willing to finance the sale themselves.

Who this is best for:

- Sellers who own free and clear and don't need all the cash at once

- Sellers who want steady monthly income rather than a lump sum

- Sellers who are concerned about capital gains taxes (installment sale treatment can spread the tax hit over years)

- Properties that might not qualify for traditional bank financing (condition issues, unusual property types)

Seller financing deals often allow for higher purchase prices in exchange for favorable terms. A seller might take $130,000 with 5% down over 10 years at 6% interest when they wouldn't take $120,000 cash — because the long-term income and interest makes it worth more to them.

Tool 3: Agreement for Deed (Land Contract / Contract for Deed)

An agreement for deed is similar to seller financing in that the seller receives monthly payments over time. The key difference: in an agreement for deed, the deed does not transfer at closing. The seller retains legal title until you've either paid off the balance or refinanced into conventional financing.

You take possession, you control the property, you have equitable title — all the practical rights of ownership. But the seller holds the deed as security until you've completed the contract.

Who this is best for:

- Sellers who own free and clear and want extra security — they keep the deed until they're paid

- Situations where the seller is nervous about creative deals and wants collateral

- Buyers who want to control a property now while planning to refinance later

Think of it like a rent-to-own arrangement, but more formal and with equitable title transferring immediately.

How to Present Creative Offers Without Losing the Seller

Here's what I do in practice: I lead with understanding. I ask the seller about their situation before I talk about any offer. What's their timeline? Do they need cash now, or is monthly income appealing? Are they worried about taxes? What happens to them if they don't sell?

Those answers tell me which structure to lead with — and how to explain it in terms that connect to their actual situation, not in terms that sound like a finance lecture.

When I present a subject-to offer, I don't say "subject to the existing financing." I say: "Here's what this would look like — you stop being responsible for the mortgage payment, I take that on, and you walk away clean." Same concept, language that lands.

Patterns for success in creative financing are built on one thing: making the seller's problem your first priority, and showing them how the structure you're offering solves it.

What to Be Careful About

Creative financing is powerful, but it requires proper legal documentation. Every single time. State laws vary. Assignment rules vary. The due-on-sale clause in subject-to deals is a real thing (though rarely triggered when payments are made consistently).

Work with a real estate attorney who has specific experience with the structure you're using. Not a general practitioner. Not a template you found online. A real estate attorney in your state who has done these deals before.

This is non-negotiable. The structure is only as good as the paperwork behind it.

Your Homework

Go back through your current leads — or start a new list if you don't have one. For each motivated seller situation you encounter this week, ask yourself these three questions:

- Does this seller have an existing mortgage, and is it a rate I'd want to keep? (Subject-to candidate)

- Does this seller own free and clear and want monthly income? (Seller financing or agreement for deed candidate)

- What's the seller's actual problem — is it money, timing, stress, taxes? — and which structure solves it best?

Then call a real estate attorney in your state this week and ask about their experience with subject-to transactions and land contracts. Know who's on your team before you need them.

If you want to go through all three creative offer structures in detail — with real deal examples, role-play practice, and live Q&A — come join the boot camp. Five evenings. Complete toolkit. 97bucks.com

Disclaimer: This content is for general educational purposes only and does not constitute legal, tax, or investment advice. Creative financing laws and regulations vary by state. Always consult a licensed real estate attorney before structuring creative financing transactions. Results vary.