5 Steps to Analyze Your First Real Estate Deal Like a Pro

Nobody Taught You How to Read a Deal

Here's what I see all the time: someone finds what looks like a promising property, gets excited, and then completely freezes. They don't know if the numbers work. They don't know what numbers to even look at. So they either pass on a deal that could have been great, or — worse — they jump in without doing the math and find out the hard way that they overpaid.

Deal analysis is the skill that separates investors who build something real from people who just talk about investing. And yet most beginner resources skip over it or make it sound like you need a finance degree.

You don't. You need five steps and the discipline to run them on every deal, every time.

Here's What Most People Do Wrong

Most new investors skip straight to the price. They look at the asking price, compare it vaguely to what they think the house is worth, and either feel good or bad about it. That's not analysis. That's a guess.

The other mistake? Only looking at the purchase price and repair cost. Those are two numbers in a much longer equation. If you're not also accounting for holding costs, closing costs, and your actual profit target, your math is broken before you even start.

Here's the thing: a deal that looks cheap can destroy your margins if the holding costs run long. And a deal that looks expensive can be a home run if your numbers are tight and your exit is solid.

You have to run the full picture. Every time.

Here's What I Do Instead

I use a five-step analysis process on every deal I look at. Doesn't matter if it takes five minutes on a quick one or an hour on a complicated one — the steps are the same. Patterns for success come from consistency, not shortcuts.

Let me walk you through each one.

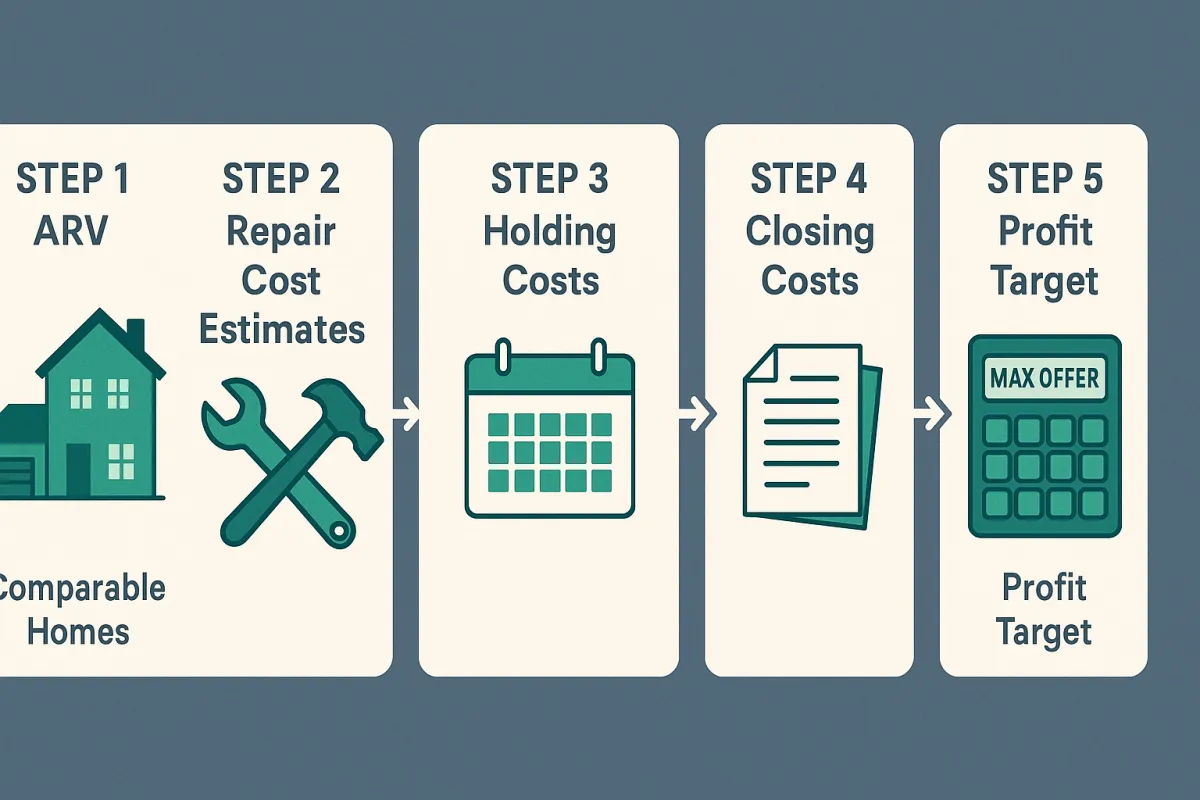

Step 1: Establish the ARV (After-Repair Value)

ARV is what the property will be worth once it's fully renovated and ready to sell or rent. This is your ceiling — every other number flows from here.

Here's what I do: I pull 3-5 comparable sales (comps) from the last 90 days within a half-mile radius. Same property type, similar square footage, similar condition after renovation. I'm not looking at active listings — I'm looking at what buyers actually paid.

Let me give you an example. You're looking at a 3-bedroom, 1,200 sq ft house in a working-class neighborhood. You find three recent sold comps that are fully updated: $185,000, $192,000, and $188,000. Your ARV is roughly $188,000-$192,000. Use the conservative end — call it $185,000.

If you can't find comps, that's a signal too. Sparse comparable sales mean an uncertain exit. Adjust your risk accordingly.

Step 2: Estimate Repair Costs Accurately

This is where most beginners get hurt. They walk through a property, see it needs a kitchen and a bathroom, and write down "$20,000 repairs." Then they find out the roof needs to go, the electrical is knob-and-tube, and there's moisture in the crawlspace — and the real number was $55,000.

Here's what I do: I walk through every system in the house. Roof, HVAC, plumbing, electrical, foundation, then cosmetic items room by room. I assign a number to each category. If I'm not sure, I bring a contractor. I'd rather spend $150 on an inspection than $15,000 on a surprise.

Use a line-item repair estimator — not a gut feeling. Then add a 10-15% contingency buffer on top of your estimate. Because something always comes up.

Step 3: Calculate Holding Costs

This is the step people forget. Holding costs are everything you pay while you own the property but before you sell or rent it — and they add up faster than you'd think.

What falls into holding costs:

- Financing cost: If you're using hard money or a private loan, you're paying interest every month. On a $120,000 loan at 12%, that's $1,200/month.

- Property taxes: Prorated by month. Don't forget this one.

- Insurance: Vacant property insurance, typically $100-$200/month depending on the property.

- Utilities: Especially if you're keeping them on during rehab for contractors.

Estimate your rehab timeline honestly, then add 30% to it. Projects run long. If you think it's a 3-month rehab, budget 4 months of holding costs.

Step 4: Add Up All Closing Costs

You have closing costs on both ends — when you buy and when you sell. Most beginners only think about the buying side, if they think about it at all.

On the buy side, plan for 2-3% of the purchase price: title fees, recording fees, attorney fees, lender fees if applicable.

On the sell side, budget 6-8%: agent commissions (if you use one), closing costs paid for the buyer, staging, any final touch-up costs, and transfer taxes.

On a $185,000 ARV deal, your selling costs alone could run $11,000-$14,800. That's real money. Don't leave it out of your math.

Step 5: Set a Profit Target and Work Backward

Now you have all your pieces. Here's how the final math works:

Max Offer = ARV − Repairs − Holding Costs − Closing Costs (buy + sell) − Profit Target

Let me give you a real example with numbers:

- ARV: $185,000

- Repairs: $35,000

- Holding costs (4 months): $6,000

- Closing costs (buy + sell): $15,000

- Profit target: $25,000

Max Offer = $185,000 − $35,000 − $6,000 − $15,000 − $25,000 = $104,000

That's your ceiling. If you can get it for $104,000 or less, the deal works on paper. If the seller wants $130,000 and won't budge, move on.

This is how you stop making emotional decisions about deals. The math tells you the answer. Your job is just to run the math correctly.

A Note on Practice

The first time you do this, it'll feel slow and uncertain. Do it ten times and it becomes natural. Do it twenty times and you'll start to see patterns — neighborhoods where repairs always run higher, seller price points that rarely work, property types where the comps are strong.

Patterns for success are built through repetition. The investors who close deals aren't geniuses. They're the ones who ran the numbers on 50 deals before they found the right one.

Your Homework

Pick one property — a Zillow listing, a courthouse lead, anything you've been sitting on — and run all five steps this week. Pull real comps. Estimate repairs line by line. Calculate your holding costs for a realistic timeline. Add your closing costs. Set a $20,000-$25,000 profit target and see what your max offer comes out to.

Then compare it to the asking price. See if there's a deal there. Even if there isn't, you'll have practiced the process on a real property.

If you want to do this live — with real properties, a group of other investors, and me walking through the analysis with you in real time — come join us at the boot camp. Five evenings. Real numbers. Real deals. 97bucks.com

Disclaimer: This content is for general educational purposes only and does not constitute legal, tax, or investment advice. Real estate investing involves risk. Consult a licensed real estate attorney, CPA, or financial advisor before making investment decisions. Results vary.