How a 1031 Exchange Works in Real Estate

How a 1031 Exchange Works in Real Estate

Folks, if you've built up equity in a rental property and you're starting to think about trading up — maybe from a single-family rental to a multi-family building, or from one market to a better one — there's a tool in the tax code that real estate investors have been using since 1921. It's called the 1031 exchange, and it's one of the most practical wealth-preservation strategies available.

Here's what it is, how it works, and where investors most commonly run into trouble with it.

What Is a 1031 Exchange?

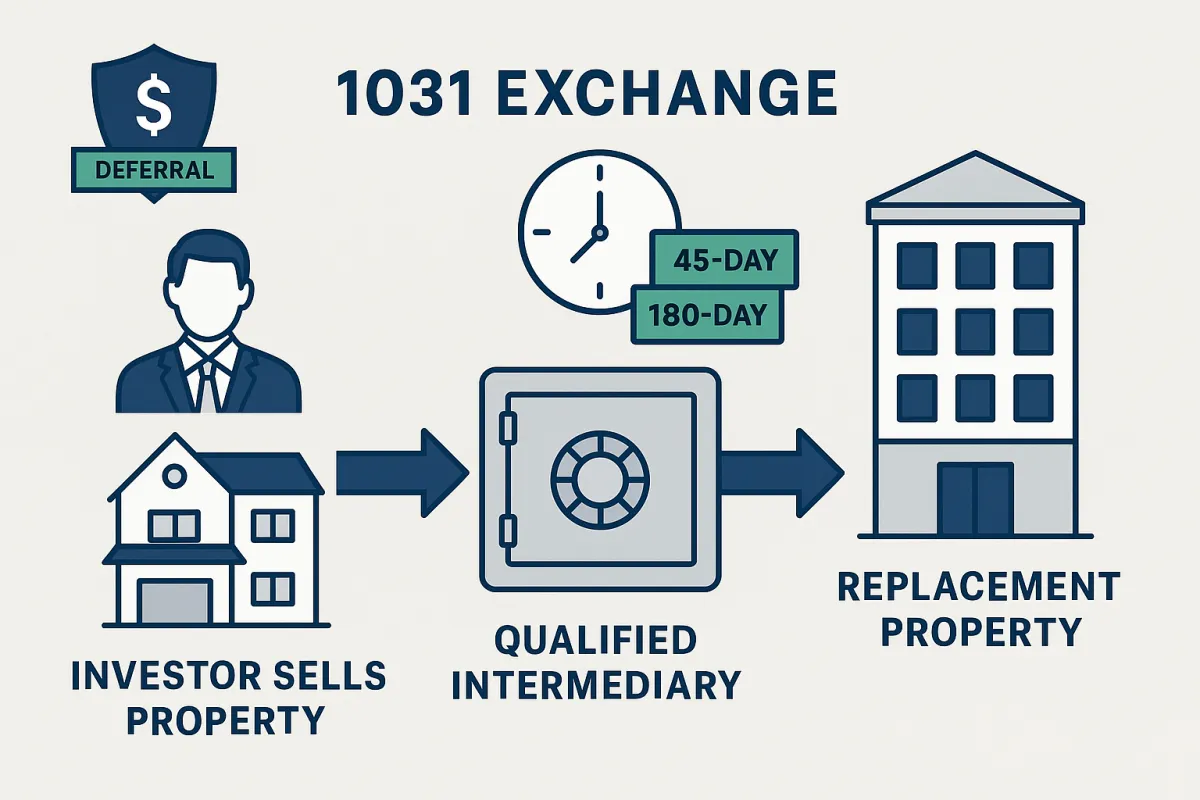

A 1031 exchange — named after Section 1031 of the Internal Revenue Code — lets you sell an investment property and reinvest the proceeds into another qualifying investment property, deferring capital gains taxes in the process.

Notice that word: defer. You're not eliminating the tax permanently. You're rolling it forward. As long as you keep exchanging into new properties, those gains continue to compound without being carved up by capital gains taxes every time you transact. Some investors defer gains for their entire investing career and pass appreciated properties to heirs on a stepped-up basis.

The practical math looks like this. Say you purchased a duplex for $180,000 eight years ago, and it's worth $310,000 today. If you sell it outright, you owe capital gains tax on the $130,000 appreciation — potentially $26,000 to $39,000 depending on your rate. With a 1031 exchange, you can roll the entire $310,000 into a larger property and keep compounding on the full amount. That difference compounds significantly over a long investing horizon.

What Qualifies as "Like-Kind" Property?

This is the part that surprises most people who are new to the concept. "Like-kind" sounds like you have to trade a rental house for an identical rental house. In real estate, it's much broader than that.

Like-kind in real estate essentially means: investment property for investment property. You can exchange:

- A single-family rental for a 4-plex

- A 4-plex for a 20-unit apartment building

- Commercial warehouse space for raw land

- A rental in Illinois for a rental in Texas

The property must be held for investment or business purposes on both sides of the transaction. Your primary residence doesn't qualify. A vacation property you use personally generally doesn't qualify either. But investment property to investment property — that's the lane, and it's a wide one.

The Two Deadlines You Cannot Miss

The 1031 exchange runs on a strict clock from the day you close on your relinquished property (the one you're selling). Miss either deadline and the exchange fails — taxes are owed for that year.

45-Day Identification Window. Within 45 calendar days of your sale closing, you must formally identify the replacement property (or properties) in writing to your Qualified Intermediary. No extensions. No exceptions for most circumstances. The clock doesn't pause for weekends or holidays.

180-Day Close Window. You must close on your replacement property within 180 days of the sale. That's 180 days total from the same starting point — not 45 plus 180. The two clocks run simultaneously.

The investors who get into trouble almost always had the 180-day window in mind but underestimated how fast the 45-day identification deadline arrives. Start identifying replacement candidates before you list your current property. Have your target properties underwritten before you need to commit to anything in writing.

The Qualified Intermediary Requirement

Here's a rule that catches people off guard: the sale proceeds cannot touch your hands at any point. Literally.

The IRS requires a Qualified Intermediary (QI) — sometimes called an exchange accommodator — to hold the funds in escrow between the sale and the replacement purchase. If the money is deposited into your personal or business account even briefly before the replacement closes, the exchange is automatically disqualified.

You need to engage the QI before your sale closes — not after. Set up the escrow arrangement before the closing date on your relinquished property. QI fees for a standard exchange typically run $500 to $1,500. Compared to what you'd owe the IRS without the exchange, that's a small cost.

One caution: QIs are not federally licensed or regulated (though some states are beginning to add oversight). Work with one that carries fidelity bonding or insurance, has a solid track record with investor transactions, and provides clear fee disclosure upfront.

Identifying Replacement Properties: The 3-Property Rule

The IRS gives you flexibility on how many properties you can identify:

The 3-Property Rule is the simplest: you can identify up to three potential replacement properties regardless of their combined value. Your final acquisition can be one, two, or all three of them.

The 200% Rule allows you to identify more than three properties, but the combined fair market value of all identified properties must stay within 200% of what you sold your relinquished property for.

Most investors working a standard exchange stick with the 3-property rule. It gives you enough flexibility to have backup options without overcomplicating the paperwork. The key is identifying properties you've already done preliminary underwriting on — not properties you're hoping might work out in time.

Boot: What Happens When You Don't Roll Everything Over

In a 1031 exchange, "boot" refers to value you receive that isn't reinvested into the replacement property. Boot is taxable.

There are two common ways boot shows up:

Cash boot. If you sold for $310,000 and only reinvested $260,000 — keeping $50,000 in cash — that $50,000 is boot and is subject to capital gains tax.

Mortgage boot. If the replacement property carries a lower mortgage balance than your relinquished property, the difference can be treated as boot. The general principle: you need to maintain or increase your debt level in the replacement, not reduce it, to avoid a taxable event.

The cleanest 1031 exchanges roll all equity forward and equal or increase the loan. Run the numbers in advance — don't discover the boot calculation at closing.

When the Numbers Make 1031 Sense

The exchange is valuable when you're scaling — when you want to trade up in property size, move into a market with better fundamentals, or diversify your portfolio, and the capital gains hit would otherwise meaningfully slow your ability to do so.

It's not always the right move. If the appreciation on your current property is modest, the transaction costs and complexity of coordinating a 1031 may outweigh the tax savings. If you genuinely need the capital for a non-real-estate purpose, the exchange constraints don't fit. And if the replacement market doesn't have properties that pencil at your required return, rushing into a deal to meet the 180-day deadline can cost you more than the taxes you saved.

Numbers are sacred. Work the full scenario — taxes owed, transaction costs, QI fees, the difference in returns between exchange and non-exchange paths — before you commit to the exchange strategy. A CPA who works with real estate investors is the right partner for that analysis, and you want to have that conversation well before you list your property.

The Bottom Line

The 1031 exchange has been in the tax code for over a century because Congress deliberately preserved the ability of investors to keep their capital at work in the economy. It's not a loophole. It's a deliberate policy tool, and it's available to regular investors, not just institutional ones.

If you're holding appreciated investment property and thinking about your next move — a larger building, a different market, a different asset type — the 1031 exchange is worth understanding in detail. Work the math honestly, get a qualified intermediary engaged early, and build your target property list before the clock starts.